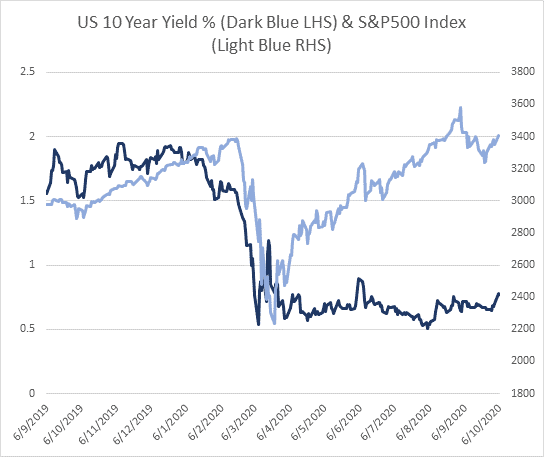

One of the key features of the recent episode is that the ~$10.5 trillion in global central bank liquidity has kept the bond term premia and credit spreads much more contained than in previous crises (relative to the GDP shock). Indeed, following the recent compression in high yield spreads, credit risk compensation in the US high yield market is back …